Olympus, on it's own is not a big problem. These things do happen. The U.S. had it's Enron, Worldcom and others.

But the problem is that Olympus is an old, stodgy blue-chip company, not some aggressive, MBA-led startup. If you can't trust Olympus, who can you trust in Japan? What other companies have similar problems? If this sort of cover-up is culturally acceptable are any of the income statements and balance sheets in Japan reliable? Is there something wrong with the auditing system in Japan? The scary part is not what happened to Olympus itself, but the suspicion that this is not uncommon (as I said, sadly, I was not surprised by what happened).

This is a scary thought for investors. This is especially true now with sentiment so fragile after the big, global financial blowup.

My fear is that this will turn people off to stocks in Japan for many years. This is not like the financial crisis in the U.S. where the collapse is easy to understand. It was a standard bubble and collapse. People now trust banks quite a bit less and are afraid of leveraged balance sheets and risk-taking financial institutions. But nobody is worried about Coca-Cola, Starbucks or Google. Yes, stocks aren't that popular after such a long period of subpar performance.

But that's different than what is going to happen in Japan going forward post-Olympus. Olympus was not a subprime lender or bank. What happened is not industry specific, so people won't just be able to avoid certain risky industries, they will have to avoid Japan overall.

The Japanese handling of the Fukushima crisis also doesn't inspire confidence. If they can't tell the truth about that, how can we trust the regulators of Japanese corporations? Would they not also lie and help cover things up for the sake of a bigger, social good?

Back in 2006 there was a Livedoor/Murakami scandal that rocked the Japanese financial markets and that really killed the Japanese OTC market, I think.

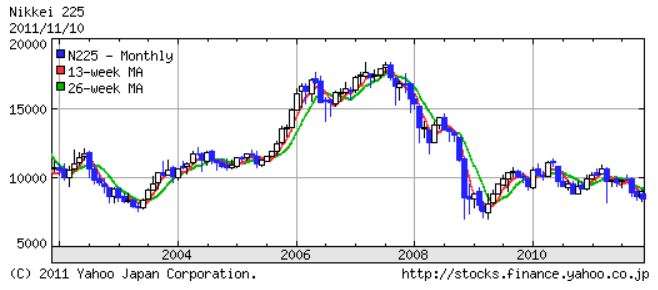

You will see that the market peaked in early 2006 just as the Livedoor scandal broke. This really turned people off to the OTC market (even though Livedoor was Tokyo Stock Exchange listed). I think it changed the perception of the market as a rigged thing with no chance for outside investors.

Why is this important? You will say that lower valuations will be good for investors and they can make good returns. This is true, but in the case of the Japanese OTC market, I think the problem is that with a bad market, low valuations and no liquidity, companies can't raise capital. If companies can't raise capital at reasonable prices, the market won't develop. I think the Japanese OTC market is stuck in the vicious cycle and can't get out of it, and it seems to me it is largely due to the Livedoor/ Murakami scandal. At least it seems like that to me.

You can see that the JASDAQ market did top out earlier than the Nikkei 225 Index. The Nikkei didn't top out until the financial crisis began to unfold.

The problem here is that any chance of people coming back to stocks in Japan may be set back for years due to this Olympus problem. Who is next? As for foreign investors, they will realize that they have no mechanism to resolve these Olympus-type problems as they do in the U.S. This means that at the margin, foreign investors will be less likely to invest in Japan.

Of course, value investors need not worry about what other people do and whether stocks are popular or not. But what it does tell you is that Japanese stocks will probably have to get a lot cheaper on a valuation basis before people get interested.

With this lack of transparency, shakey accounting/auditing, no recourse when trouble occurs, rational investors will demand a discount to invest in such a place.

For many years, Japanese stocks traded at a premium to U.S. and other global stocks. This really made no sense to me as returns on capital, margins and other productivity measures were usually far lower than Western counterparts.

The premium has disappeared in the past couple of years making people bullish on Japan again, but Olympus, I think, will change that somewhat. Parity valuation will not be a reason to go to Japan anymore (unless there are other factors that make a specific investment interesting. All of these things have to be evaluated on a case-by-case basis).

Couple that with the incompetence of the Japanese government in dealing with the economic situation and government finances, this is a recipe for a long, extended bear market far longer than has already occurred.

This is very unfortunate as I have been interested in Japan for many, many years and have been waiting for some sort of bottoming out over there.

It now looks like there won't be a true bottom for a long time.

I will continue to look for interesting situations over there, but things are not looking too good at all.

I do also understand that I may be putting in a low in the Japanese stock market by making such a negative post!

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.