Anyway, with News Corp breaking up (after repeatedly saying it's not going to happen) and many calling for the big banks to break up, I thought it's a good time to look at BAC as a potential spin-off/ potential stub / sum-of-the-parts.

You know people will keep denying things until the day before something happens (remember Goldman Sachs? Nope, we will not become a bank. Next day, um, well, yes... we are now a bank, lol...)

I don't agree with the many people calling for breaking up banks that are too big to fail and too complex to manage but BAC is one bank where I would tend to think that wouldn't be such a bad idea.

In any case, a spin-off may not happen; the first quarter resegmenting of business units seems to make it more unlikely it will happen than not. But who knows.

Doing this exercise, though, will shed some light on what this beast really is made of so even if we come up with a similar sum-of-the-parts valuation as the "1% ROA for the whole firm" valuation we will have a little deeper understanding of the components that make up that value.

Use 2011 Year-end

Starting with the first quarter of 2012, BAC rejiggered their business segments. They used to report two segments that were pretty much the old Merrill Lynch (with some old BAC tossed in); Global Banking and Markets (GBM) and Global Wealth and Investment Management (GWIM).

In the 1Q 2012, they broke up GBM into two parts again, Global Banking (GB) and Global Markets (GM). This is what they used to report a while back too, but for most of the time after the Merrill acquisition, it was reported as one segment, GBM.

That's all fine, but the problem is that when they broke it up again, they stuck some of the Global Commercial Banking into Global Banking. The GB and GM together now is bigger than GBM back in 2011.

So instead of using the most up-to-date figures, I will use the data from 2011 year end as that is reported with the old segments. Judging by their 1Q earnings report, there hasn't been anything dramatic so it shouldn't make too much difference analysis-wise.

How is the old Merrill doing?

So first of all, since we are focusing on the old Merrill and the hypothetical spin-off scenario, we need to look at how they are doing. I will ignore what Merrill did before the crisis as it's a different world now.

So I decided to just take a look at how they have done since the crisis. Since there aren't a lot of data points, I just looked at the quarterly figures. Maybe I am tricking myself into thinking I have more data points by using quarterly, but at least I get to see more of what's going on inside this way.

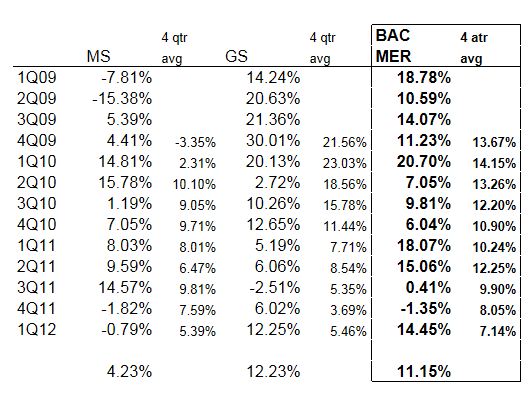

Here is the Return on Average Equity (ROAE) of what I call BAC-MER or the old Merrill Lynch compared to Morgan Stanley (MS) and Goldman Sachs (GS), the only two large independent investment banks. I also included a four quarter average ROAE so we can see trends.

Return on Average Equity

I took out some one-time figures from the BAC ROAE figures. In the second quarter of 2009, BAC-MER's GBM unit had a $3.8 billion gain on a joint venture with First Data, and in the fourth quarter of 2009 the GWIM segment booked a $1.1 billion gain on the sale of Blackrock (The BLK stake was later moved to "Other" so I don't think the sale of the rest of it went through GWIM).

So in that sense, the BAC-MER figures should be pretty clean. I may have missed a gain here or there, but I think the two above were the big ones.

I didn't do the same for MS or GS; they are as they were reported so may include gains and losses here and there.

But anyway, it's very interesting to look at this table. Since 2009, BAC-MER has earned an ROAE of 11.15%, solidly in the double digits; not far from what GS was able to achieve. We can sort of see why MS is so cheap; it has only earned 4.2% in ROAE since the first quarter of 2009.

(DVA adjustments are included in all of these figures; GS is known to 'hedge' out there DVA volatility to minimize earnings impact from credit spread changes).

On a rolling four-quarter basis, it even looks like BAC-MER is doing better than GS (never thought I'd ever type that!) since the 1Q 2009. In the full year 2011, BAC-MER had an ROAE of 8.4% versus GS's 3.7%.

So despite the nightmare of BAC, BAC-MER is doing fine and is even doing better than GS.

Valuation of BAC-MER versus Comps

The problem with a sum-of-the-parts now is that investment banks are trading pretty cheap too. Since MS is doing horribly, let's compare BAC-MER with GS.

Using current stock prices and balance sheet values as of the end of March 2012, here is the valuation for BAC-MER comps:

Stock Tangible

price BPS P/B BPS P/TB

MS $13.51 $30.74 0.44x $27.37 0.49x

GS $91.00 $134.48 0.68x $123.94 0.73x

MS is not doing too well, so is trading pretty cheap. But GS is doing well, sort of like BAC-MER, but it is trading at 0.7x book. For valuation purposes, I would argue that a business earning double digit ROE's deserve to trade at book, particularly when the business is in a depressed state.

Let's see if I can find some support for valuing BAC-MER at book value. Here is a table showing the book value per share (BPS), tangible book value per share (TBPS), stock price, P/B ratio and P/tangible book ratio for GS in the recent past.

GS Stock Valuation: Quarterly Since 1Q2009

We see that even after the crisis, GS has averaged around 1.2x P/B ratio and around 1.0x P/B if you look only at the past eight quarters. It has averaged around 0.8x for the past four quarters, though.

In any case, just by looking at this table it is not a stretch to see that these banks, if they earn double digit ROE's over time, they should be valued at or over book value. The problem in the past few quarters is that there was the European crisis last fall that has continued this year. So these valuations may reflect 'crisis' or 'fear'-based valuations.

Of course, there is always the possibility that the world will in fact end soon in which case all is moot.

Another way to look at this:

GS has traded at an average 0.84x P/B ratio in the past four quarters while it earned an average ROAE of 5.5% during that time. BAC-MER, however, in the past four quarters earned an average ROAE of 7.14%, 1.3x times higher than GS. Yes, it feels strange to say that BAC-MER has done better than GS, but there it is.

So let's say a fair valuation for BAC-MER is 1.3x what GS has traded at. That comes to 1.1x P/B (1.3x 0.84x = 1.1x).

GS has also traded at 1.0x book for the past eight quarters while it earned an ROAE of 6.6% during that time. BAC-MER has actually earned an average ROAE of 8.6% during that time, or 1.3x better (this is getting really weird to keep typing that). It would not be at all surprising if BAC-MER then also traded at 1.3x book over that period.

Yes, I know that sounds like I'm really reaching here. But I'm just trying to justify book value for BAC-MER, not trying to get the highest valuation or anything like that (I'm not an investment banker representing a seller).

So looking at it in the following ways, you can easily justify valuing BAC-MER at book value:

- A business earning double digit ROE over time should trade at book or more, and BAC-MER has earned double digit ROE since early 2009. If one concludes that the current crisis is cyclical and not a permanent situation, then it's reasonable to assume that they will continue to earn double digit ROE over time, in which case book value is a reasonable valuation.

- GS has earned double digit ROE since 2009 and has averaged a valuation of 1.2x book. Even excluding the perhaps overly exuberant 2009 rebound valuation, it averaged 1.0x book over the past 8 quarters. BAC-MER has done at least as well (8.6% ROAE for BAC-MER versus 6.6% for GS), so a 1.3x book value valuation would not be out of the ordinary.

- In the past four quarters, GS has averaged a valuation of 0.84x book value while earning an ROAE of 5.5%. BAC-MER has averaged an ROAE of 7.1% so it would not be unreasonable for BAC-MER to be valued at 1.1x BPS.

- Of course, many will insist on using current valuation and not some average valuation. GS currently trades at a P/B ratio of 0.68x book, so even using current depressed valuations, BAC-MER can reasonably be valued at 0.9x book (0.68 x 1.3x).

What's the Stub Worth?

So if we back out the old Merrill, what does that leave and what's the valuation there?

Here are the basic figures:

GBM GWIM Total BAC-MER

Total assets (period-end): $637.8 bn $238.8 bn $921.6 bn

Average equity: $37.2 bn $17.8 bn $ 55.0 bn

Average economic capital: $26.6 bn $7.1 bn $ 33.7 bn

(I use average allocated equity and economic capital because that's what reported in the filings; any difference between that and period-end shouldn't change the conclusion. Economic capital is basically tangible equity.)

At year-end 2011, there were 10.5 billion shares outstanding and the stock is trading currently at $7.60/share for a total market cap of $79.8 billion.

Backing out BAC-MER at book, that leaves a market cap of $24.8 billion. On a per share basis, BAC-MER is worth, at book, $5.24/share, and the rest of BAC is valued at $2.36/share.

So what do you get for $24.8 billion?

Backing out the above capital and assets from the consolidated BAC will leave the balance sheet excluding BAC-MER:

Consolidated BAC-MER BAC ex-MER

Common equity: $211.7 bn $55 bn $156.7 bn

Tangible equity: $133.1 bn $33.7 bn $99.4 bn

Total assets: $2,129 bn $921.6 bn $1,206.4 bn

So BPS and tangible BPS of BAC excluding the old MER would be $14.92/share and $9.47/share respectively versus the market valuation of $2.36/share.

That values BAC at 0.16x book value or 0.25x tangible book value. I know most people believe that the goodwill from the Countrywide acquisition is worthless, but management is guiding ROA of the whole firm at around 1.0% (including BAC-MER).

Since BAC-MER has a much lower ROAE, this implies that BAC excluding BAC-MER will have an ROAE higher than 1.0%.

So even assuming a 1.0% ROA for the core BAC, that implies profit potential of $12.06 billion/year or $1.15/share. At 10x p/e, that's $11.50/share for the core BAC. Combining that with BAC-MER being worth $5.24/share, BAC as a whole is worth $16.74/share versus the current price under $8.00/share.

(You can also say that $12.06 billion/year is a 12% return on tangible book and and say core BAC is worth at least that. Tangible book value per share for the core BAC is $9.47/share, adding MER back to that gives $14.71/share in value for BAC overall).

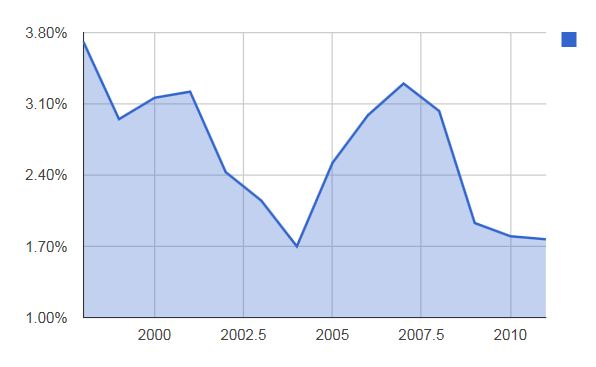

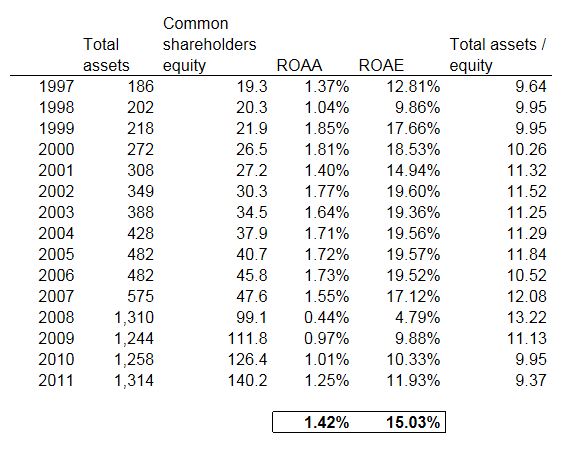

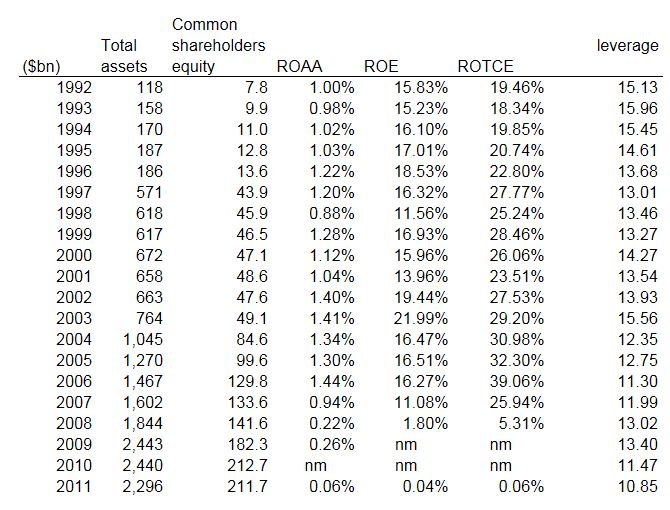

Just to check that, the following table shows the long term ROAA, ROE and ROTCE over time for BAC.

BAC Summary of Returns

So it seems like in more normal times BAC does consistently earn ROAA over 1.0% and can be as high as 1.3-1.4%. BAC has morphed over the years through multiple mergers, so I actually don't know how relevant some of the older figures are. For most of these years, BAC didn't have MER (which was added to BAC in the first quarter of 2009) so it's a good indication of what the core BAC may earn.

But what we can say is that it seems like they earn sufficient ROE to merit trading at book. You will notice that the leverage of BAC has come down over time. Reduced leverage will certainly lower return on equity, but even at a lower 10x leverage and a 1.0% return on assets (BAC management's goal and Berkowitz' valuation assumption), that is a 10% ROE.

At this point, excluding BAC-MER, core BAC's leverage is down to 7.7x, and a 1% ROA would result in a ROE of 7.7% so that's on the low side. The question is if BAC is holding back on leverage due to BAC-MER, or if they spun it off if they can lever back up to 10x.

A conservative view, though, would be to see the core bank worth at least tangible book.

To get to core BAC being worth book value, one of two things would have to take place: Leverage has to get back to 10-1 with ROA at 1.0% or ROA would have to get back up to 1.3%. From the above ROA table, you can see that BAC hasn't earned 1.3% ROA in the 90s, but did so in the 2000s. But that includes the bubble years so it's hard to tell what BAC can do over time on a normalized, non-bubble basis.

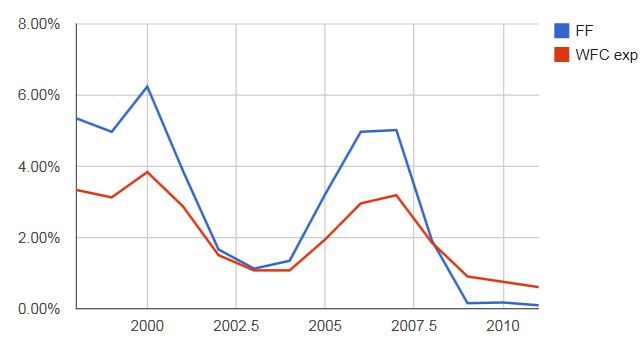

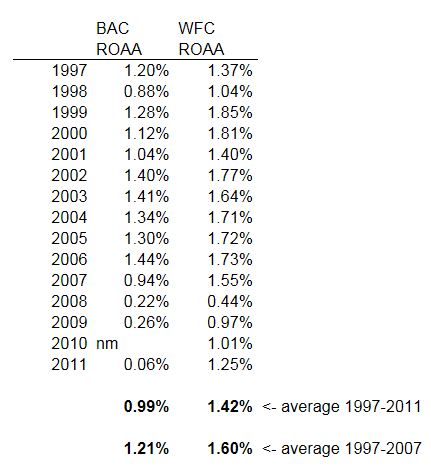

Comparing Core BAC and WFC

One reference point may be WFC. BAC excluding BAC-MER would look pretty much like WFC. Of course, WFC is way better managed, but Buffett owns both of them and thinks that BAC's underlying businesses are doing fine.

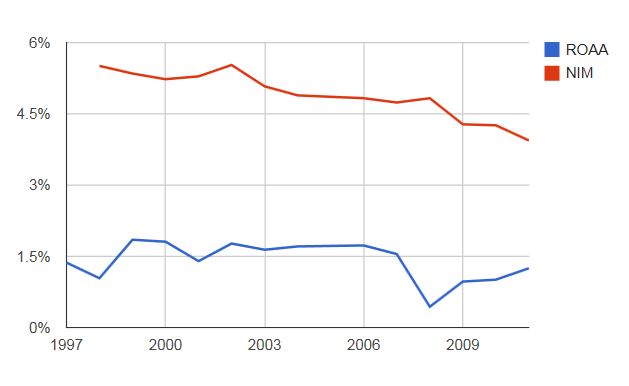

Anyway, I put the ROA of both companies side by side to see if what WFC is earning can be a hint to what BAC might earn:

The interesting thing here is that although BAC has a history of earning well over 1.0% ROA, it has been consistently lower than WFC even before BAC bought MER. The average ROA since 1997 for BAC is 0.99% versus 1.42% for WFC (actually, if you include a negative number for 2010 for BAC, it would be lower, but I am being generous here by leaving out 2010 which isn't even fair).

Excluding the bust, we get the same result. BAC averaged 1.2% ROA versus 1.6% for WFC in the ten years 1997-2007.

So unless we get a full recovery (including housing) in the U.S. economy, BAC (ex-BAC-MER) may not earn much above 1.0% ROA in which case the valuation for BAC ex-BAC-MER would be worth around tangible book or slightly more, but not stated book.

Review of the Simple Model for BAC Valuation

Berkowitz's valuation for BAC is simply that BAC can earn 1.0% ROA and with 10x leverage can earn an ROE of 10% so is worth book value, which at the end of 2011 was $20.09/share (tangible BPS was $12.95/share).

BAC in their presentations also present a base case "normalized" earnings scenario of at least 1% ROA.

If we go backwards, backing out BAC-MER at book value, we can figure out what kind of ROA the core BAC will need to earn to make a 10% ROE (to justify being worth book value).

Since BAC-MER (investment bank etc.) typically earns a far lower ROA than the core bank, in order for BAC as a whole to earn 1%, the core bank needs to earn a higher than 1% ROA.

We have already seen above that in order for core BAC to be worth book value, core BAC would have to either increase leverage (assets) 30%, or earn a ROA of 1.3%. I don't know if BAC can grow assets 30% in this environment; getting to ROA through restructuring, costs cuts etc. might be more manageable.

But that is still not an easy thing to do given the historical ROA (see above table), the fact that BAC has consistently earned an ROA 30-40 bps lower than WFC.

Conclusion

In any case, either way you look at it, BAC does seem pretty cheap. We looked at the two main pieces and I would be comfortable with the conservative assumptions, but the $20/share value might only be achievable in a broader economic recovery, especially housing.

It is encouraging that WFC is doing so well with 1.25% ROA with housing still flat on it's back, so BAC with a similar model (perhaps not as well managed) should be able to earn 1.0% ROA even without a housing recovery. In that case, a $16.74 or so would seem completely reasonable (valuing BAC-MER at book value for the reasons I stated above and assuming a 1.0% ROA on the core BAC, valued at 10x p/e). This valuation would not offend me, and I would tend to think it's conservative.

If you insist on giving an investment bank a 30% discount like the current GS (even though I would argue that since MER is doing better, they might need only a 10% discount), you can just knock off $1.60 (since BAC-MER is worth $5.24/share at book) from the above $16.74. That would still get you to $15.14/share versus the current stock price of $7.60/share.

Of course this is not to say that BAC as a whole can't earn an ROA of 1.0%; BAC suggests they can do that on a normalized basis with no asset growth (implying no real housing recovery?).

So BAC may very well be worth $20 or more.

But picking apart the details, at least we know it can be worth at least $15.00 using our own assumptions (or $14.74/share with BAC-MER at book and the rest at tangible book).