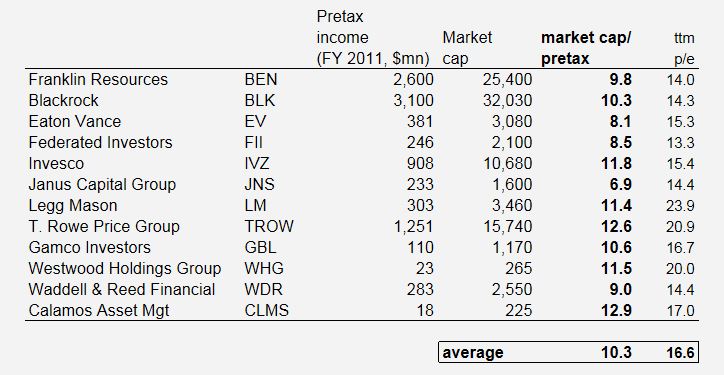

OK, so I mentioned WisdomTree Investment (WETF) in my last post. In my other post looking at DoubleLine, I sort of got a feel for what money management firms are worth. I got comfortable with the fact that asset managers currently trade for around 10x pretax profits and that's pretty consistent across asset manager types.

Here's the table from that

post (as of August):

Asset Manager Valuation

Asset Manager Operating Margins

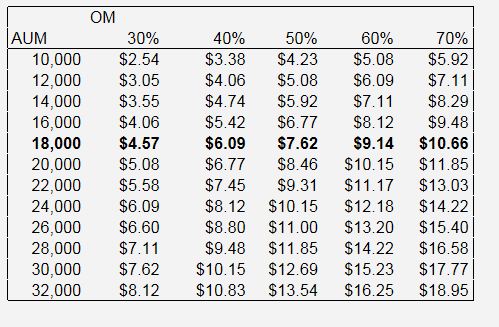

Also, using the same universe of asset managers, I took a quick look at what the operating margins typically are. If we can get a handle on that, then we can pretty much value any asset manager. I think this is better than using percentage of assets under management (AUM), which varies greatly according to type of assets (equities, fixed income, money market, alternative), fund type etc. (hedge funds vs. mutual funds etc.).

So here are some figures I plucked from the various 10-K's for the last five years. Surprisingly, operating margins seem pretty consistent across the board and even over time. It does seem to be a pretty great business. I would've expected more margin volatility, particularly after what happened during these years.

Operating Margins

The TTM (trailing twelve month) margin, I pulled off of Yahoo finance. If it differs greatly from my own figures, it may be because I used "adjusted" margins if managers provided that in their 10-K's, and Yahoo Finance may have used GAAP reported figures.

But in any case, it looks like asset managers typically earn 30%-ish operating margins.

With 30% operating margin assumptions and a 10x pretax multiple valuation, we only need to know AUM and average management fee rates (and maybe some sub-operating income line items) to figure out what an asset management is worth.

Now that I have this hammer, let's take a look at this WETF nail.

WisdomTree

So what is WETF? I don't intend to go through the whole history, but the short story is that this used to be Jonathan Steinberg's publishing company. The publishing business was called Individual Investor Group and it published the Individual Investor magazine, a magazine Steinberg bought with his family's money. It was delisted in 2001 and came back to NASDAQ recently (you can see some of their annual reports during the unlisted years at otcmarkets.com. Older 10-K's before delisting can be seen at sec.gov) after changing into an ETF manager.

Who is Jonathan Steinberg?

Jonathan Steinberg is the son of the famous corporate raider, greenmailer or whatever you want to call him, Saul Steinberg. You can google him up and read all about him. I don't know that much about him but he doesn't have the greatest reputation. I leave that judgement to others. Johathan is also knows as CNBC's Maria Bartiromo's husband.

I also knew him (not personally) through his TV commercials on CNBC advertising his Individual Investor magazine.

Anyway, Steinberg went to Wharton but dropped out in 1988 to buy the magazine (which was a penny stock magazine with a different name). He ran this business which included other publications and an investment management business (a hedge fund, apparently) called WisdomTree Capital Management which was shut down in 1998. Steinberg also published a book called Midas Investing: How You Can Make 20% in the Stock Market This Year and Every Year. The book was published in 1996, and his hedge fund was shut down in 1998, so apparently whatever he wrote in that book doesn't work.

Just browsing through some of the 10-K's, it looks like this company (Individual Investor Group) never made money. They don't have 10-K's going back that far, but just from what is there, the company has lost money in every single year from at least 1994 all the way through 2000.

So this is the baffling part. He bought the magazine in 1988 and there was the biggest bull market in history since then all the way to the year 2000 and his company never made any money. His hedge fund didn't work out. How can that be?

Looking at the filings post 2001 shows that WETF lost money every single year from 2004 through 2010 too. 2011 was the first profitable year. So as far as we know, 2011 might have been the first profitable year for Steinberg in 23 years. There was one year that had an extraordinary gain, and there may have been some profits in the years that are missing filings (and pre-1994), but even still, that's an astonishingly long, consistent record of losing money.

It is a bit surprising for a guy that was apparently into stocks as a kid. He bragged in one article that he was the only 13-year old with a Value Line subscription.

So on that basis, this is not someone you would want to be investing with.

Jeremy Siegel

So somewhere in this story is Jeremy Siegel, professor at Wharton School of the University of Pennsylvania. He was in the TV commercials advertising the WisdomTree funds and is an advisor to WETF. The story is that Steinberg shopped this idea to him and he thought it was such a great idea that he signed on. Well, this may well be true because it does sound like a good idea.

But upon further investigation, I realized that Saul Steinberg was a huge donor to Wharton School; there's a Steinberg Hall and a Steinberg Conference Center and a Saul P. Steinberg Professor of Management chair.

Saul Steinberg is still on the Board of Overseers at Wharton. Ron Perelman and James Tisch (of Loews) are on the board too. (Totally irrelevant, but Jonathan's sister was once married to Jonathan Tisch).

Siegel was also a regular contributing columnist to the Individual Investor magazine (as was, understandably, Maria Bartiromo).

So this sort of dilutes the impact of Siegel's endorsement (not that it would carry much weight to begin with; an endorsement from academia doesn't carry much weight in the world of finance, I don't think, particularly when they are considered the Irving Fisher of the 2000 bubble (Irving Fisher is the economist who said in October 1929, right before the crash, "Stock prices have reached what looks like a permanently high plateau". Siegel was calling for stocks for the long term. To be fair, Siegel only talked about stocks for the long term, not for the next five, ten or twenty years).

Michael Steinhardt

So obviously one has to wonder where the Steinhardt connection comes in (Steinhardt is a hedge fund legend). I don't have any particular knowledge but it's probably safe to say that there is some Saul connection here too. Steinhardt and Saul Steiberg are around the same age and they are both Wharton grads, so perhaps that's where the connection is.

Even still, I don't know if Steinhardt, who owns 25.4%, or 31.7 million shares as of the latest proxy, would put his reputation on the line and so much capital for something that he doesn't think is going to work. At $6.80/share, that amounts to more than $200 million. That's a lot of money even for a rich hedge fund legend. Of course, Steinhardt probably paid way less than that.

There are some filings missing during the unlisted years so I really have no idea what he paid (in December 2006, WETF sold 18.8 million shares for $56.5 million in proceeds, which comes to $3.00/share, but that may not have been Steinhardt. It could have been another of the large holders (Robinson)).

Of course, Steinhardt's involvement is no guarantee of success either.

In February 2012, Steinhardt did sell 6.2 million shares in total for $5.33/share in the secondary offering, so either way, he is in liquidation mode. This also isn't necessarily a bad sign. Of course shareholders would probably prefer he keep the stock, but it's not unusual for these angel investors to get out once the stock is listed and trading and out of the initial venture stage.

Insider Selling

A quick look at insider transactions does seem to show that WETF insiders have all been selling this year. This may not be a good sign, but since WETF was just listed on the NASDAQ and many employees including Steinberg had (and has) many options, it is understandable that they would exercise and take some cash out. Again, this isn't that unusual for a newly listed venture business (which WETF essentially is even though it has existed in a different business/form since 1988).

So anyway, that's sort of the history and background of this entity.

Let's look at the business itself, which is what I am interested in.

The Business

OK, so let's not worry too much about the past and focus on what the current business is all about. WETF is basically an ETF manager that manages fundamental-weighted portfolios. As I already mentioned, the stock weightings are decided by dividends, earnings or some other factor. I think WETF is mostly dividends or earnings.

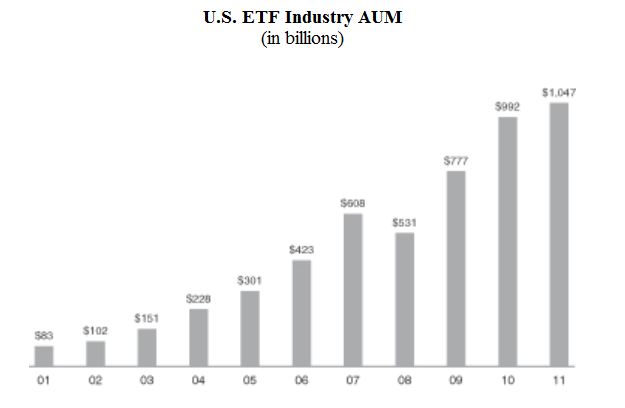

Anyway, here is a look at the growth of the ETF industry (from the WETF 2011 10-K):

As you can see, the ETF industry has seen tremendous growth since 2001. Even after the financial crisis, the ETF industry has snapped back with AUM far exceeding the 2007 high. That shows you how much money has moved into ETFs from individual stocks and mutual funds (some of this also may be non-equity ETFs, international ETFs etc).

Of course, this increase in the ETF business is not entirely a good thing; there are so many ETFs listed now that it is remininiscent of the go-go mutual fund years of the late 90s when veteran Wall Streeters complained that there were more mutual funds than individual stocks. Sometimes it seems like the ETF industry is now getting there (maybe there are 1,500 ETFs listed now?).

The good thing about ETFs is that it is low cost and for the most part passive; most people are better off indexing. But the bad thing is that the beauty of indexing has sort of been defeated by the boom in indexing; now there are so many indices and ETFs, how do we know where to invest? The whole point of indexing is to be totally passive and not make those decisions. With so many indices and ETFs, it is just as hard or harder now to decide where to put your money.

Not only that, since the ETFs are so low cost and very liquid (for the bigger, liquid ones), it does encourage trading. In fact, I suspect most ETFs are used for trading and speculative purposes and not really investing (money managers trading the SPY because they don't want to trade futures etc...). It is so ironic that the idea of indexing came from a passive, low cost approach, but now the ETFs are used so much for short-term trading/speculative purposes.

But anyway, I think the move towards ETFs will continue and AUM in the sector will continue to go up, but the number of funds may at some point peak out as a lot of smaller ETFs may not survive. If the cost of keeping them going is minimal, they may survive just so the ETF managers can have a full line of product, but I don't know. I just can't imagine the number of ETFs going up forever.

WETF AUM

So frankly, this is the thing that got my attention. WETF is run by a guy that hasn't really been successful in anything he has tried so far; I would not put my money with him.

But here's what got me a little bit interested. The AUM at WETF has been growing nicely:

The AUM is up to $15 billion as of the first half of 2012. I think this is closer to $17 billion now as of September (I don't think WETF publishes AUM monthly).

Here is the distribution of that AUM:

Here is the ranking of ETF managers as of December 2011:

AUM %growth

1. iShares $448 bn +0.3%

2. State Street $267 bn +7.6%

3. Vanguard $170 bn +14.7%

4. PowerShares $45 bn + 7.7%

5. Van Eck $23 bn +17.7%

6. ProShares $23 bn +1.4%

7. WisdomTree $12 bn +23.2%

8. Deutsche Bank $12 bn +3.7%

9. Rydex $8 bn +3.4%

10.Direxion $7 bn +1.8%

As of the end of 2011, 85% of the equity ETFs that WETF has out outperformed their benchmark indices since inception. They launched their first ETFs in June 2006. I think that figure is 74% or so now as of the end of June, 2012. This may fluctuate over the short term.

Here is the AUM of WETF versus the S&P 500 and some other indices:

WisdomTree AUM versus S&P 500 and other Major Indices

So this is pretty good. They are accumulating assets at a pretty good pace.

You can see the performance of the various WETF funds

here. I tend to think even with five years, it's a bit too short a time period to evaluate the funds.

What is WETF Worth?

At the top of this post, I said that we can value an asset manager using a 30% operating margin and 10x pretax earnings.

Here are the average management fees for WETF for the last three years:

Average fee

2009: 0.52%

2010: 0.56%

2011: 0.55%

average: 0.54%

The fees, despite the competition seems to be stable. But let's just use 0.50% for fees. This may trend down over time with increasing competition. But for now, let's just use 0.50%.

They have close to $17 billion in AUM now, so that's $85 million in revenues. At a 30% operating margin, that's $25.5 million in operating income.

As of the end of June, 2012, there was around 139 million diluted shares outstanding, so that comes to $0.18/share (don't forget, this is not EPS; it's pretax earnings per share). 10x this figure is $1.80/share. But wait, there is some cash, investments and tax deferred assets.

Also, I used diluted shares outstanding but didn't include the cash that would come in from exercised options (there are some options with exercise prices slightly above current price levels, but for simplicity I will include them; besides, the breakdown by exercise price is not in the Q). Of the 16.6 million dilutive shares, 14.9 million of that is from options with an average weighted exercise price of $0.94/share. If that was exercised, that would add $14 million in cash to the WETF balance sheet.

So here are the other items:

(per share)

Cash and cash equivalents: $39.3 million $0.28

Cash from option exercise: $14 million $0.10

Investments: $9.8 million $0.07

Deferred Tax Assets: $49 million $0.35

Total: $112.1 million $0.80

Some of the cash may be offset by current liabilities and some cash is needed to run the business, but let's be generous here and just include it all. WETF has no long term debt or other long term liabilities.

This $112 million comes to $0.80/share.

So adding that back to our above $1.80/share gives us a value of $2.60/share for WETF. WETF is now trading at $6.74/share, so on a steady state basis with $17 billion of AUM, WETF is certainly not cheap at all and would in fact be an interesting short.

BUT WAIT! This is actually not correct. This is a start-up business with AUM ramping up, so WETF at this point doesn't have the scale to be that profitable. So using a 30% margin on $17 billion AUM doesn't work.

If that's the case, if AUM stays at $17 billion, it would be worse than the above analysis as WETF wouldn't be able to earn a 30% margin. I tend to like businesses where it makes a whole lot of sense as is and any growth would be a bonus. WETF is certainly not in that category.

When Will WETF Become More Solidly Profitable?

So this is a key question. At what AUM level would WETF earn 30% operating margins? Steinberg mentioned in the 2Q 2012 conference call that he thinks WETF can earn a 40% operating margin at $40 billion in AUM, a much lower level than his competitors due to the small, low cost operation he runs.

WETF AUM is in fact growing at a nice pace:

WETF AUM growth

2009 +87%

2010 +65%

2011 +23%

2012 YTD +40%

So maybe WETF gets AUM up to $40 billion within the next few years.

Let's redo the above figures using $40 billion AUM and 40% operating margin, and then adding back the balance sheet items like deferred tax asset, cash etc.

$40 billion of AUM and 0.50% average fees would generate $200 million in revenues and $80 million in operating income. With 139 million shares outstanding, that's $0.58/share. At 10x pretax earnings, WETF's ETF business is worth $5.80/share.

Adding back the above balance sheet items of $0.80/share, that's $6.60/share.

So if we snapped our fingers and magically got WETF AUM up to $40 billion now and it can generate 40% operating margins (which is not unreasonable given my above table of asset manager margins), WETF would be worth

$6.60/share.

The stock is currently trading at $6.75/share so the market is already discounting WETF achieving a $40 billion AUM.

In order for this to be a buy, you have to assume that WETF continues to grow AUM beyond that at a nice pace. Using the above assumptions, WETF would be worth $15/share with an AUM of $100 billion. Can it get there? I don't know, but it won't be easy. If this concept really takes off, I don't think there really is a moat, and any of the other larger ETF managers can launch similar ETFs. And over the next few years, there may be pressure on fees as they compete for assets. This is what happens in any market when it gets saturated (as the ETF business seems to be getting).

Alternative Valuation Approach

Blackrock paid $13.5 billion for iShares, which I think came to 4.5% of AUM at the time. By that measure WETF would be worth $5.50/share. I think someone said that Invesco paid 7% or 7.5% of AUM for Powershares, but the deal was based on some complicated formula-based contingent payments so it's hard to say what the real price was. Using 7.5% AUM, that would value WETF at over $9.00/share.

[ Correction on October 2, 2012: Someone pointed out in the comments below that in fact the Blackrock acquisition came to 0.8% of AUM, not 4.5% because BGI had $1.8 trillion of AUM at the time. The 4.5% figure is based on the AUM at the time for iShares, not all of BGI which included iShares ]

WETF is certainly growing AUM at a high rate for now, so any acquisition will probably come on the high side. I have no idea what Steinberg / Steinhardt's thoughts are on acquisitions (selling), but I would imagine that they would want to sell at one point when it gets big enough so they can cash out. I wouldn't be surprised if Steinhardt would want to sell, having ridden this to success from nothing while Steinberg may not want to, finally having a successful, profitable entity to run.

The problem is that the cost for existing ETF managers to create their own fundamental-weighted index ETFs would probably be much lower than buying out WETF (as I can't imagine any fund management industry board of directors desperately wanting the services of Steinberg).

I really don't have a view on that. Maybe someone who doesn't have an ETF business would be interested.

If WETF started to buy stuff, though, I would be a little concerned given Steinberg's history.

Research Affiliates Litigation

Oh, and there is one more thing. Research Affiliates is suing WETF for using their idea of fundamentals-weighted indices.

I really don't know much about law, so take this with a grain of salt, but I find it hard to believe that something like this can be patentable, or enforceable in court. Can you really patent how to weight an index? And if you did, is it really enforceable in court? Yes, you can copyright an index. I can see that.

I've dealt with derivatives over the years, and the industry copies each other all the time. When there is one derivatives structure that works well, everyone else copies (credit default swaps or convertible bond asset swaps, for example). I don't have a particularly good memory, but I don't recall ever having to pay a license fee or anything like that.

Even for listed products, I think at the time, all you can do was get a trademark or servicemark on something and hope nobody uses the same exact name for something (like the Brooklyn Investor Fundamental-Value-Weighted Index Warrants Series A (don't hit it up on Bloomberg; it doesn't exist!)).

(I think DECS and PERCS were listed derivatives products that were copyrighted or servicemarked; you can't use the name "DECS" or "PERCS", but you can create a product with the same structure).

Does the Dow Jones Company have a patent on price-weighted indices? Who owns the VWAP idea (volume weighted average price)? What about exponential moving averages? Who did that first? (do we care?)

So my impression is, if this concept of fundamental weighted indexing is ownable by someone, I would be very surprised.

But again, I remind you that I don't really know the details of the lawsuit; I only read what's in the 10-K about it and haven't seen any legal / court filings, so don't read this and go, "whew, we don't have to worry about this lawsuit".

Conclusion

I do like the concept of fundemental-weighted indices and value-weighted indices for the reasons Greenblatt explained in his book. I also like the asset management business for the reason I stated before; the economics can be better than owning the funds themselves (operating leverage, revenue growth boost from asset net inflows etc.). This looked like a good candidate to fulfill both. WETF is the only listed pure-play ETF manager out there.

But upon taking a closer look, it doesn't look too great at this point. Unless of course you really think WETF can get their AUM to $100 billion and beyond. If that happens, of course, this can very well work out.

I tend to think, though, that if WETF does continue to grow AUM and it gets to $40, $50 billion, then the other big competitors will obviously take a closer look at this idea. I don't think there is anything WETF is doing that the other larger competitors can't do. They have the infrastructure and distribution to be able to do the same thing, probably even better (as some of them have research collaborations with academia/research institutes).

Anyway, I will stay away from this one for now but will keep an eye on it for sure.

Here are my thoughts in summary:

- This is not a management I would be comfortable with. With something like OAK, I don't worry about management at all. But Jonathan Steinberg has failed to make money since 1988 during the biggest bull market of all time so it is a bit worrisome. If WETF gets bigger, at some point Steinberg might want to step aside and let someone with experience (and more credibility) run the business and he can become chairman/visionary or whatever. He can still retain a large ownership and pay himself well. I would not sleep well at night if I had a lot of money in a company run by Steinberg, frankly.

The most important thing here, though, is price. WETF already fully discounts a business with $40 billion in AUM and 40% operating margin (versus the current $17 billion in AUM). But this is growing quickly so this may not be a problem for growth investors. I like to buy stuff that is interesting now and we get the growth for free (or cheap).

Increasing competition from bigger entities will certainly come if WETF keeps growing assets. At $10-15 billion, they can be ignored, but not if they get bigger. This would also put pressure on fees going forward.