Here are the relevant websites:

http://www.frmocorp.com/

http://www.horizonkinetics.com/

FRMO is a strange entity, but basically it owns a stake in Horizon Kinetics (asset manager), has cash and investment assets, revenue sharing stream and things like that. More on that later.

Horizon Kinetics is an asset manager run by Murray Stahl and Steven Bregman. Murray Stahl sounds like an outsider's outsider. Or maybe that's outsider^2. He loves owner-operator businesses which is similar to the outsider CEOs and he himself is a manager (of funds, FRMO and Horizon Kinetics) who thinks like an outsider.

Check out how "outside" he is in his thinking. This is a snip from a recent conference call transcript (on the website: FRMO might have the best investor website ever. Even better than Berkshire Hathaway and Leucadia; it has the simplicity of each of them, but includes conference call and annual meeting transcripts!)

Value Investor Insight (May 31, 2013)

Anyway, at the website there is a great interview with him from Value Investor Insight (May 31, 2013).

Here are some notes from that interview:

- Stahl quote: "Every perspective I have will sooner or later go stale... I'm constantly looking for how successful people do things differently."

- Horizon Kinetics manages $8.1 billion; the large cap strategy has returned +11.5%/year net versus 7.6%/year for the S&P 500 index since January 1996.

- Likes owner-operated businesses. Warren Buffett and John Malone are examples.

- Leucadia is also an example. Handler looks good so still owns Leucadia.

- Sears is another example and the story there is not over yet.

- Valuation methodology: estimate earnings in four or five years, apply reasonable multiple and then discount back at 20%. If implied discount rate is greater than 20%, will look at closely.

These are some names discussed in detail:

- Brookfield Asset Management (BAM); has owned for a long time, trading below liquidation value, spin-off opportunities

- Dreamworks (DWA): market not giving credit to film library; market tends to price stock based on most recent movie (hit or not).

- Ascent Capital (ASCMA): Malone spinoff. Burglar alarms, fragmented industry, opportunity for accretive acquisitions etc. Amortization obscures core profitability (at $73.50) trading at 7-8x forward free cash.

- Likes Oaktree Capital Group (OAK): Run by Howard Marks. Look at PIMCO (AUM $2 trillion) for potential upside of DoubleLine (AUM $60 billion).

- Dundee Corp: Canadian owner-operator. Analogous to Brookfield and Leucadia. Run by Ned Goodwin. Sum of the parts play.

- Onex Corp: Listed private equity firm in Canada. Trading at value of investments; market giving no value to management company (fee revenues streams).

Anyway, you will notice that this manager seems right up my alley. He likes the same sort of companies that I do for similar reasons.

Owner-Operators

Since we are on an outsider CEO kick now, this is really on-topic to what I've been looking at recently (and another reason why I'm making this post).

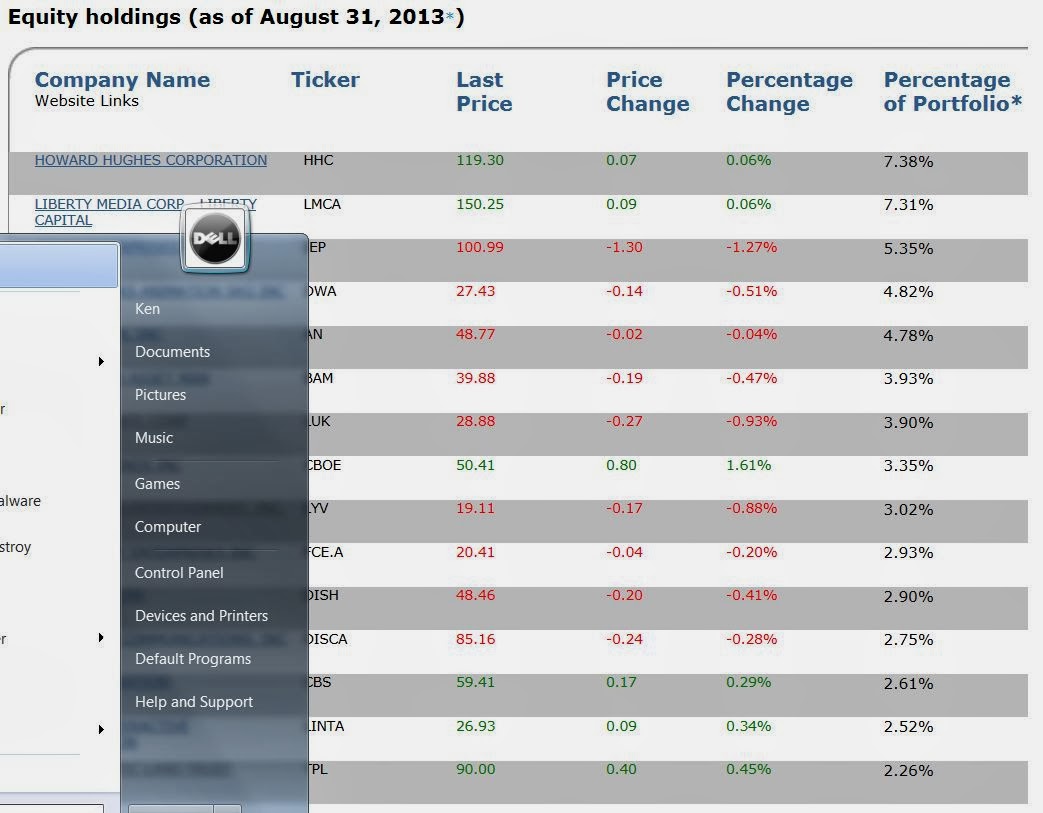

Check out the holdings of the Kinetics Paradigm funds. With $1.2 billion in AUM, I guess it's one of the main funds that Horizon advises:

So check this out. It is a pretty focused fund (compared to other mutual funds) and there are a bunch of owner-operator and spin-off/special situations stuff. I'm surprised more people don't talk about Murray Stahl / Horizon.

How has this fund done over the years?

All of this and more is available at the Kinetics Mutual Funds website.

So even if you don't invest in mutual funds, at the very least, checking out the holdings here is not a bad idea.

But anyway, back to the topic of owner-operators.

Stahl talks a lot about the problems of indexing in the annual reports, annual meeting and conference calls. So I think in an act against this trend, he has created his own index. He decided to create an index based on owner-operated businesses instead of creating a fund or ETF. You can read about all the reasons why in his literature, but at the end of the day, he just decided that that's the best way to go; it can be objective (third party to calculate / manage the index) and the cost of creating an index is very low (pencil, paper and a calculator). Revenues that accrue from licensing will therefore have high returns.

Anyway, this lead to the Wealth Index.

Horizon-Kinetics ISE Wealth Index

This index is based on Stahl's idea that owner-operated businesses tend to outperform over time. Again, I really recommend people to go read all of the annual reports and read the annual meeting transcpripts at the FRMO website. He offers investment ideas and things like that too (at the annual meeting). And it won't take long. It's not like reading the 10-K of J.P. Morgan for the last ten years or anything like that at all. In fact, you can read all of that stuff in less time it takes to read a JPM 10-K for a single year.

Anyway, the index is composed of companies run by wealthy people in control positions.

Here is how it has done over time:

Not bad at all for a mechanical index.

So let's take a look at the inside of this thing. Here is just a sample list:

So look at that. Some of our favorite names are in there. Berkshire Hathaway, Colfax (subject of a recent post), Loews, Liberty Media, Greenlight, Google, Vornado, Sears etc...

If you had an algorithm to pick stocks, you can do worse than this.

Going off on a tangent for a second; how about taking this index as a basket and then applying the Magic Formula to it, or 'value'-weighting it as Greenblatt suggests? Then you might get some insane returns. But then again, some of those metrics may not work for the above names.

At the annual meeting (according to the transcript), they said they have a new wealth index for the Japanese market and they are also developing a similar idea based on spin-offs.

There's a whole lot more and I may post more about what I find later. There is still a bunch of stuff on the website (like research) that I haven't dug into, but from what I've read so far, I bet they would be well worth any serious value investor's time.

FRMO Corp

OK, so finally I get to FRMO.

I'm not going to go through the history here. Stahl explains it well in the documentation at the website. If I attempt to summarize it, I will probably bungle it and confuse everyone. So let's just say that all sorts of things happened at FRMO over time, and now the structure may be a little more stable going forward.

I think in the past it used to be really tricky to value this because FRMO had an ownership stake in a private entity (Horizon Kinetics) that didn't disclose much information. If someone owns 1% of something and you don't know what that something is in terms of financials, you can't value it.

That's still sort of the case, even though we know a little more. I think Stahl said that more will become public over time. For example, the revenue share stream became clear starting in the first quarter of the new year because the non-investment related revenue will be pretty much the revenue share from Horizon-Kinetics (they get 4.199% of Horizon's revenues).

They also own 4.95% of Horizon Kinetics itself. So we have two problems; what is the Horizon revenue sharing stream going to look like, and what is Horizon-Kinetics worth?

I have some ideas about that and I may post something at a later date.

But for now, I have a cheap copout on this. Since they just did the deal where FRMO's ownership of Horizon Kinetics went up 4.09% to 4.95% we can use that as a valuation benchmark. The deal was done on May 2013 so it's still fresh, or maybe five months old at most.

[ By the way, I found a typo on page 12 of the 2012 year-end financial statements. At the bottom of the page, the dates May 31, 2012 and May 31, 2013 should be reversed; Investment in Horizon Kinetics LLC is marked at $10,973,940 as of May 31, 2012 instead of May 31, 2013. ]

Valuation

I don't think there was any mention at the 2013 annual meeting of the valuation of the deal in May when FRMO acquired 4.09% of Horizon-Kinetics, but I think they did it at what they consider fair value. The last time they did a similar deal (mentioned in the 2012 annual meeting), Stahl said that they priced the deal using other asset managers as comps to avoid a conflict (as Stahl runs both FRMO and Horizon). I think he said they used 6.3x EBITDA for the earlier deal excluding some stuff on the balance sheet. That was when AUM and valuations were depressed in the sector, he said.

Assuming they did the same this time in May, then the $11 million valuation on the balance sheet for the Horizon Kinetics stake might not be too far off. I have no idea what the balance sheet capital is at Horizon Kinetics so this is probably low (in the earlier deal, the balance sheet assets were not included in the valuation so FRMO got it for free). But if they did the transaction at a fair price using asset manager comps, then the May 31, 2013 valuation might not be a bad benchmark going forward.

As for the revenue share stream, it is also booked at around $10 million. This is also a 'fresh' mark, so even if it's at cost, it hit the book recently from a fresh valuation. This value was "determined by an independent valuation" so it may not be as good as the 4.95% ownership stake.

If I recall correctly, I think Stahl said that in the first quarter of this year (no conference call transcript of 1Q14) we will see the revenue stream; basically what is not investment related revenues should be the revenue sharing revenues. If that is correct, then the revenue stream is $680,000 in the first quarter which annualizes to $2.7 million. Using a 10% discount rate gets you a value of $27 million for this stream. Using a 6% discount will get you to $45 million. Either way, it's a lot larger than $10 million on the book. This is pretax, but from an earlier post about asset managers, I am comfortable with 10x pretax earnings as a valuation for asset management earnings streams.

As for equity income from the 4.95% ownership, I thought Stahl said that we would see that itemized in the 1Q earnings report, but it looks like the income is clumped together with the investment partnerships as "Income from investment partnerships and limited liability companies". They have $19 million or so of investment partnerships interests on the balance sheet so we don't know how much of this income is from the investment partnerships and what is from Horizon Kinetics.

So unless I am missing something, we still don't have enough information to get a value for Horizon Kinetics; the best guess is still where they did the transaction in May ($11 million).

What is curious is that both the 4.95% equity stake and 4.199% gross revenue sharing agreement are marked at a very similar level of $10-11 million. As they mentioned before, a gross revenue sharing agreement is worth more than an equity interest as revenues don't come with costs attached (where an equity holder will get less than revenues due to expenses).

So my tentative conclusion is, let's say the 4.95% equity stake in Horizon is worth what it's on the books for ($11 million) and the revenue sharing agreement is worth much more. From the above (if the assumption is correct that "Consultancy and advisory fees" is all from this agreement), then it may be worth $17 - $35 million more than the $10 million it's stated at on the balance sheet. With 43 million shares outstanding, that comes to $0.40- $0.80 per share more than stated book value.

The rest of book value is cash and investments, which are all marked to market.

So with shareholders equity at $1.93/share as of the end of August 2013, and an additional value of a possible $0.40 - $0.80, that's an adjusted value of $2.33 - $2.73. But using my 10x pretax value for the revenue share stream, it may be closer to $2.33 (But keep in mind that this revenue stream can grow alot from here).

That makes the current stock price a bit high at $6.90/share.

Let's say that the equity value of Horizon Kinetics is actually very understated, even if they did the May transaction at what they themselves (Stahl) felt was fair value. As a sanity check, let's assume that the 1Q revenue share income annualized of $2.7 million is more or less normal and they have (now or eventually) 50% operating margins (TROW, PZN and other equity and alternative managers have margins in that area).

But with the revenue sharing agreement, the operating margin would be 46% (they have to pay out 4% of revenues so 50% - 4%). Horizon would have annualized revenues of $64 million and at 46% operating margin gets you pretax earnings of $30 million, and 10x that is $300 million. 4.95% of that is $14.9 million, or another $0.09 on the balance sheet ($11 million is already on the balance sheet). That would give us a total range of $2.42 - $2.82/share as the fair value of FRMO. There are other adjustments to be made, but this is just a big picture guestimate.

Anyway, this back-of-the-napkin Horizon Kinetics value is probably way off as we don't know what the fee structure details are. As I mentioned before I'm not a big fan of percentage of AUM as a valuation measure either as that really depends on the underlying assets (equities versus bonds versus liquidity funds), structure (mutual fund-like fixed management fee, institutional/retail, advisory / subadvisory, hedge fund-type fee with incentives etc...) and other factors. 10x pretax earnings seemed to work well the last time I looked; valuations are probably higher now.

But!

If you read the annual reports and conference calls, you will notice that they have a lot of new projects planned, many with very low marginal cost (hedge funds, more indices and services with swaps which is very interesting to me as I have been involved with derivatives before (I assume they just get the licensing fee and not have anything to do with any actual swap)). There can be a lot of potential there. We don't know what the margins are at Horizon, but if new projects stick, they can probably get some pretty good operating leverage that is not reflected in the valuations above. Licensing fees literally just fall straight to the bottom line and there won't be any AUM associated with that either.

They also said that AUM growth is accelerating (or at least the Horizon revenue growth).

Either way, this stock isn't currently trading at below any "readily ascertainable asset value" but who knows. I look forward to following this going forward.

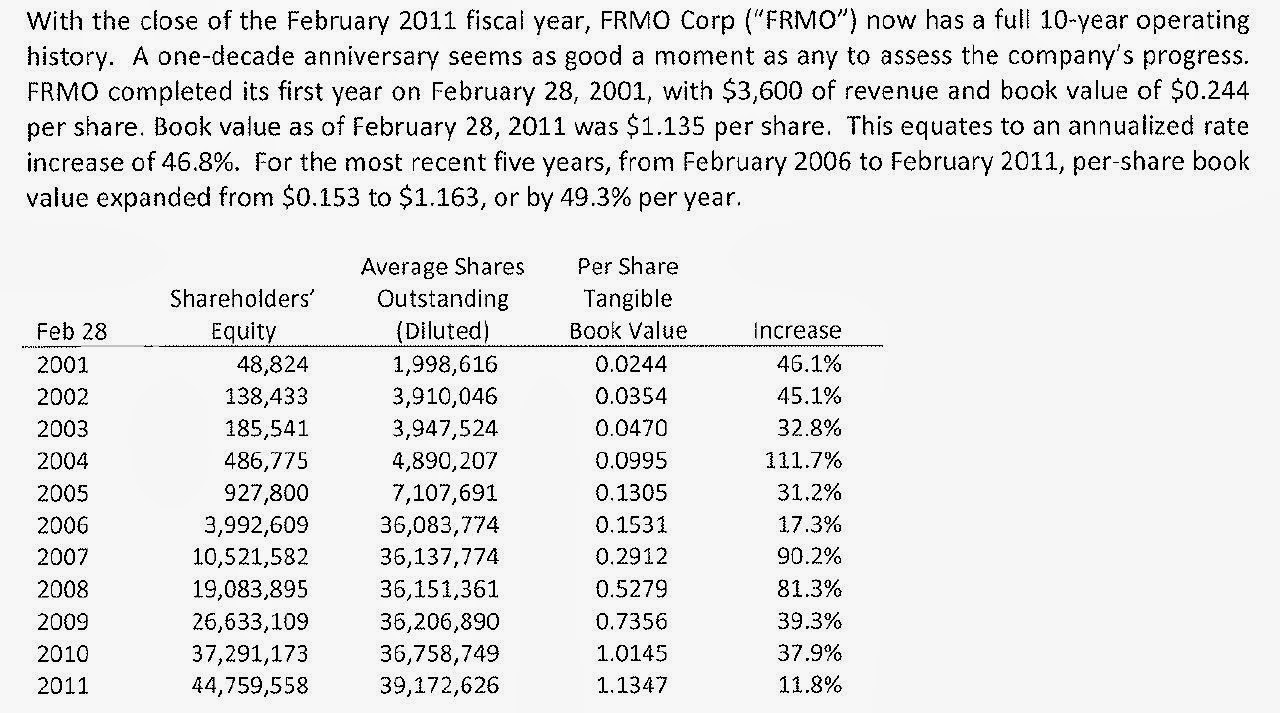

By the way, the structure of FRMO has been evolving and equity base is getting bigger so this may not be indicative of future potential, but check out the history of growth in per share value of FRMO over the years from their 2011 letter to shareholders (per share tangible BPS was $1.39 and $1.93 for 2012 and 2013):

{kind=link}