That's mostly because I thought there was an alternative asset bubble and I wasn't that excited about prospective returns from some of these guys who have grown their assets so quickly in the past few years. Every presentation you look at, you see these alternative managers growing AUM at a double digit clip. And then you have to wonder, all of these guys at some point have to fish in a smaller and smaller pond (as their asset base gets bigger, they have to pursue bigger deals). What will happen to returns when so many giants are chasing the same, small number of fish?

I sort of still feel this way, but Och-Ziff Capital Management (OZM) caught my attention because I've always liked their approach and mix of strategies. I was sort of surprised to see that they are diversifying into real estate and credit. OZM is not really completely market neutral, but they are known for hedged strategies in equities; risk arbitrage, convertible arbitrage, equity long/short etc. So that is sort of the appeal at OZM; they are not bull market dependent, and they outperform in down markets.

Adding real estate and credit makes them less so, even though Och has said in a conference call that he doesn't think that is the case. Well, for a while if you are doing only really special situation deals, that is probably true, but as you get bigger in the area, you can't not start to correlate to some extent with the real estate/credit markets. Plus, I think OZM is concerned with correlation with the S&P 500 index. In that sense, yes, adding credit and real estate may not increase correlation to the index (except in bear markets/crashes when everything goes down!).

12% Dividend Yield?!

Anyway, what hit my radar is that OZM is now trading at around $8.60/share, and their dividends for the past twelve months is $1.03/share; that's a 12% dividend yield. That certainly looks appealing in this market.

Since 2008, dividends average around $0.91/share, so OZM is trading at a 10.6% yield to average dividends since 2008. Again, looks good.

Returns at OZM's Master fund wasn't that inspiring at 5.5% net last year. I think investors expect (or used to) 10%. I hope OZM still shoots for double digit returns. In 2013 when the fund returned 13.9%, dividends were $1.79/share. If OZM had a similar year again, that's a potential 21% dividend yield (but read on before getting too excited). Anyway, if we normalize earnings for a 10% return we can figure out what normalized earnings would be going forward.

As of the end of June 2015, OZM had AUM of $48 billion. Their management fees as a percentage of average assets (using the average of beginning of the year and end of year AUM) averaged around 1.6% since 2003. But their growth in credit in real estate has caused that to come down some. The average management fee in 2Q2015 was 1.42%. So let's just use 1.4% for now.

Management fee with $48 billion in AUM gives us $672 million in revenues. 20% incentive fees on 10% return would give us $960 million in incentive fees and total revenues of $1.6 billion. Economic income margins have averaged around 67% since 2003, but more like 61% since the IPO. In good years, like 2013, the margin would be higher (67%) due to higher incentive fee income, and in so-so years like 2014, lower (60%).

So let's use 60% economic income margin to be conservative. That gives us $960 million in economic income. Using a 20% tax rate (average of last three years), that gets us to distributable income of around $770 million. With 516 million shares outstanding (using average adjusted shares outstanding for 2Q15), that's $1.50/share in distributable income. Since OZM tends to pay out most of their distributable income, that would be a 17% dividend yield on a normalized basis.

Pretty nice, and conservative too.

But Wait!!

So my first pass at looking at this was kind of exciting. But then I realized it's not so simple. I noticed that their cash bonuses tends to be around 20% of total revenues every year, and that sounded a bit low. As most of us know, at these alternative asset managers, anything from 40-60% of incentive income is actually paid out to the fund managers.

OZM earned around $1 billion in incentive fees in 2013, but only paid $316 million in cash bonuses. This includes bonuses for non-investment managers, so seems a little low for an alternative manager.

But look at what's not included in the economic income calculation: in 2013, OZM granted 12,470,271 RSU's and 24,097,722 Group A Units at fair values of around $10.00 at the time of grant. That's $366 million of pay to employees that doesn't hit the economic income line. So the economic income margin is sort of bogus.

Total bonuses are more like $682 million, which comes to 42% of total revenues and 63% of incentive income. That makes more sense.

Total Share Count

Of course, we don't have to look at all that to realize this. All you need to do is track the total shares outstanding over time to see what's going on. I won't get into the details of the various share classes; I'll just focus on what OZM calls the adjusted class A shares.

These are the weighted average outstanding for the respective years:

million shares

2008 400

2009 404

2010 410

2011 419

2012 455

2013 482

2014 509

Over the past six years, shares outstanding have grown 4%/year. The above dividends per share already accounts for the growing number of shares outstanding so you don't have to deduct 4% from the 10% dividend yield.

In 2013, around 37 million shares were granted (RSU and Group A units) at a fair value of around $10.00. Let's say they repurchased those shares at the grant-date fair value to keep shares outstanding flat for 2013. This would have cost $370 million. Distributable earnings in 2013 were around $900 million. Instead of paying out dividends, if $370 million was used to repurchase shares, distributable earnings would go down to $530 million. If we use the 455 million shares outstanding of 2012 (since this is the weighted average for the year, it would be higher for full year 2013 even if they granted no new shares), that would get us to distributable earnings per share of $1.16/share.

So, if OZM has another great year like 2013, that would give us an actual yield of 13.5% ($1.16/$8.60). Not bad at all, but not the 20% we saw above.

2014 wasn't a great year in terms of returns (+5.5% net for the main fund), but not bad on an AUM growth basis. One can argue a $1.07/share dividend in a so-so year on a $8.60/share stock price is not bad at all; a 12.4% yield. Last year only 10 million RSU's were granted (and no Group A Units), so adjusting this would only reduce the possible dividend to $0.95/share or so, for a not so bad 11% yield.

Normalized @ 10% Return

Let's go back to my above example and normalize distributable earnings with a 10% return for OZM's funds. Using AUM of $48 billion, management fee rate of 1.4%, 10% return on the funds and a 20% incentive fee rate, we got total revenues of $1.6 billion. We then used an economic income margin of 60% for economic income of $960 million, and then a 20% tax rate to get to $770 million in distributable income.

But this figure excludes stock compensation expense. I don't really care if it is included in earnings or not; if we want to assume shares outstanding to stay the same (share repurchase to offset dilution), this would reduce available cash to distribute to shareholders and that's what we sort of want to know. Who cares what GAAP says, or what the amortization rate on expensing this stuff is.

I don't know the formula for paying out stock compensation, but one of the most consistent ratios is stock compensation expense (my definition, not OZM's) to total economic revenues. Here, I use stock compensation expense as the total fair value of RSU's and Group A units granted (on grant date).

Looking at that versus total revenue (segment, or economic revenue):

Fair value of grants / total revenue

2010 11.9%

2011 11.6%

2012 10.4%

2013 22.5%

2014 10.5%

It looks fairly consistent at between 10-12% except for 2013, which was a good year performance-wise. Well, 2012 was good too. I'm not sure why 2013 stands out. There may be a good reason for this, but I couldn't find anything as I went through the conference calls and things like that.

Anyway, I will use 12% stock compensation in my normalized distributable earnings scenario.

So, we got up to $770 million in distributable income. We know from the above that total revenues is $1.6 billion, so total value of equity grants would be $192 million. Deduct that from our distributable income gives us real distributable income of $578 million. With 516 million shares outstanding, that gives us $1.12 in distributable income per share. That's still around a 13% yield; pretty nice, but not the big upside we thought earlier.

If, however, stock grants go up again, this would be much lower; if they granted stock worth 20% of total revenues, distributable income would drop to $0.87/share for a yield of around 10%.

Oddly enough (or not), there doesn't seem to be a huge difference implying that when OZM does really well, the upside is 'granted' away off the income statement.

Doing all of the above again with 65% economic income margin, we would get $1.24 in normalized distributable income for a 14.4% yield. This could be lower if more stock was granted (here I only use 12% of revenues as the value of stocks granted).

I may be missing some things here and there. I know there are class D stocks, and to offset the above RSU/Group A Units, there are cancellations and forfeitures. But it doesn't really change the big picture of what's going on here.

Also, I haven't modeled into the above the longer-term assets under management; some AUM are invested for three to five year terms and incentive fees are realized and booked as revenues at the end of the term. As of the end of June 2015, there were $16.5 billion (34% of total AUM) of such assets with accrued incentive fees (but not booked as revenues) of $353 million. I haven't modeled this in the above so actual margins may be higher than I suggest. But if this has been going on for a while, the incentive fees would actually be included in the historical figures as some funds may already have come to term (old funds come to term, revenues are recognized etc.); 6% and 17% of longer-term AUM will come to term in 3Q15 and second half of 2015 respectively.

In any case, all of this is very rough as it is tough to model.

OZM Fund Performance

Anyway, OZM is not a bad investment if you like this sort of thing (and I know many do not). There are the usual concerns of size (can they keep performing as they get bigger?), diversification (Carlyle Group's blunders in hedge funds etc...), strategies getting crowded as alternative funds all seem to be growing their AUMs at rapid rates, perpetual-low-interest-rate-high-valuation-tight-spreads-low-return environment etc...

Anyway, let's look at some earlier performance figures. OZM really did perform well until recently.

This is from their 2007 10-K and you can see how amazing OZM figures were:

| 1 Year | 3 Years | 5 Years | Strategy Inception | |||||||||

Net Annualized Return(1)

| ||||||||||||

OZ Master Fund, Ltd.(2)

| 11.5 | % | 11.7 | % | 13.9 | % | 16.5 | % | ||||

S&P 500 Index

| 5.5 | % | 8.6 | % | 12.8 | % | 11.0 | % | ||||

Correlation of OZ Master Fund, Ltd. to S&P 500 Index(3)

| 0.60 | 0.60 | 0.57 | 0.45 | ||||||||

Volatility(4)

| ||||||||||||

Master Fund Standard Deviation (Annualized)

| 3.8 | 3.1 | 3.3 | 5.0 | ||||||||

S&P 500 Index Standard Deviation (Annualized)

| 9.7 | 7.8 | 8.6 | 14.0 | ||||||||

Sharpe Ratio(5)

| ||||||||||||

Master Fund

| 1.63 | 2.30 | 3.16 | 2.41 | ||||||||

S&P 500 Index

| 0.01 | 0.50 | 1.09 | 0.47 |

They outperformed the S&P 500 with low correlation to the market and with much lower volatility.

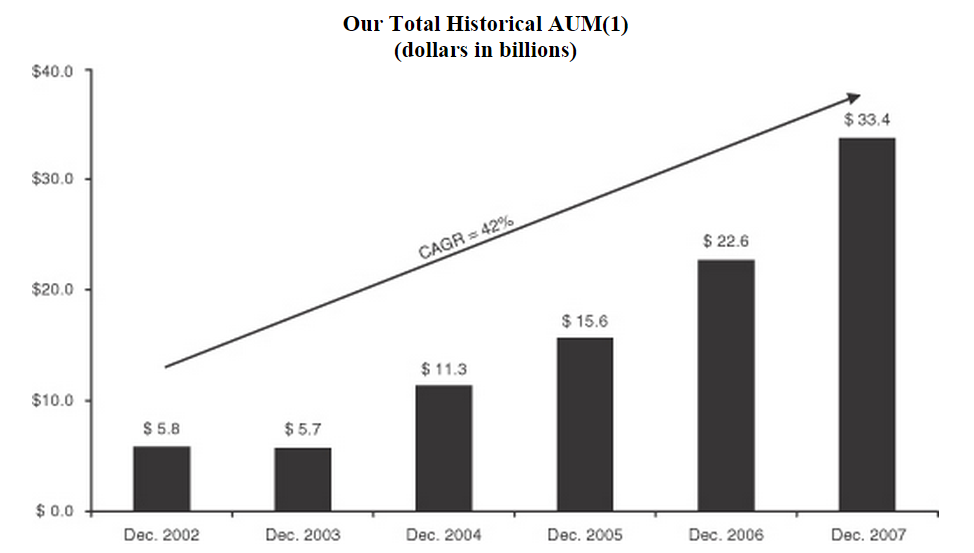

Here is the AUM growth chart from 2007:

Net Annualized Return through December 31, 2014

|

1 Year

|

3 Years

|

5 Years

|

Since OZ Master

Fund Inception

(January 1, 1998)

|

Since Och-Ziff

Multi-Strategy

Composite

Inception

(April 1, 1994)

| |||||

OZ Master Fund Composite(1)

|

5.5%

|

10.3%

|

7.7%

|

9.6%

|

n/a

| |||||

Och-Ziff Multi-Strategy Composite(2)

|

5.5%

|

10.3%

|

7.7%

|

9.6%

|

12.8%

| |||||

S&P 500 Index(3)

|

13.7%

|

20.4%

|

15.5%

|

6.5%

|

9.8%

| |||||

MSCI World Index(3)

|

10.4%

|

18.5%

|

11.8%

|

5.6%

|

7.4%

| |||||

Volatility - Standard Deviation (Annualized)(4)

| ||||||||||

OZ Master Fund Composite(1)

|

5.0%

|

3.6%

|

3.8%

|

4.9%

|

n/a

| |||||

Och-Ziff Multi-Strategy Composite(2)

|

5.0%

|

3.6%

|

3.8%

|

4.9%

|

5.4%

| |||||

S&P 500 Index(3)

|

8.3%

|

9.1%

|

13.0%

|

15.6%

|

15.0%

| |||||

MSCI World Index(3)

|

7.2%

|

8.9%

|

11.9%

|

14.7%

|

14.1%

| |||||

Sharpe Ratio(5)

| ||||||||||

OZ Master Fund Composite(1)

|

1.08

|

2.82

|

1.99

|

1.42

|

n/a

| |||||

Och-Ziff Multi-Strategy Composite(2)

|

1.08

|

2.82

|

1.99

|

1.42

|

1.80

| |||||

S&P 500 Index(3)

|

1.64

|

2.22

|

1.17

|

0.25

|

0.44

| |||||

MSCI World Index(3)

|

1.43

|

2.07

|

0.97

|

0.20

|

0.30

| |||||

_______________

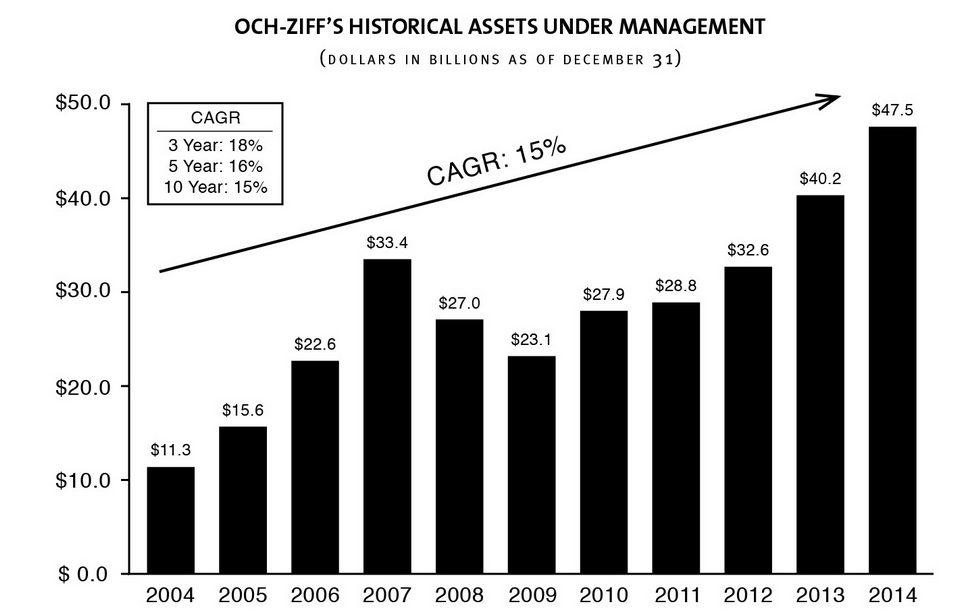

Not so exciting anymore. And the AUM chart looks like this:

Here's a table that shows yearly returns for OZM's fund going back to 1994. You can see that a lot of the high returns were achieved in the early years. Look at those returns from 1994-2000! And when the market tanked after the internet bubble, they did pretty well preserving capital.

But since 2000, OZM only returned around 6%/year, but that's still better than the 4%/year of the S&P 500 index (total return). Since the 2007 peak (to look at 'through-cycle' performance), OZM returned around 6%/year versus the 7.3%/year for the S&P 500 index.

| OZM fund | S&P500 | |

| 1994 | 28.50% | 5.30% |

| 1995 | 23.50% | 27.40% |

| 1996 | 27.40% | 23.00% |

| 1997 | 26.70% | 33.40% |

| 1998 | 11.10% | 28.60% |

| 1999 | 18.80% | 21.00% |

| 2000 | 20.60% | -9.10% |

| 2001 | 6.30% | -11.90% |

| 2002 | -1.60% | -22.10% |

| 2003 | 24.00% | 28.70% |

| 2004 | 11.10% | 10.90% |

| 2005 | 8.80% | 4.90% |

| 2006 | 14.80% | 15.80% |

| 2007 | 11.50% | 5.50% |

| 2008 | -15.90% | -37.00% |

| 2009 | 23.10% | 26.50% |

| 2010 | 8.50% | 15.10% |

| 2011 | -0.50% | 2.10% |

| 2012 | 11.60% | 16.00% |

| 2013 | 13.90% | 32.40% |

| 2014 | 5.50% | 13.70% |

| 5 year avg | 7.68% | 15.46% |

| 10 year avg | 7.64% | 7.68% |

| Since 1994 | 12.68% | 9.24% |

| Since 2000 | 5.97% | 3.86% |

| Since 2007 | 5.95% | 7.28% |

Low Returns

It seems like they had great returns back in the old days when they had AUM under $10 billion, They got their AUM over $10 billion in 2004, and since then their return has been around 7.6%/year.

Part of it is no doubt due to size; when you are bigger, you can't capitalize on the smaller opportunities. There is no doubt about that regardless of what anybody says. The bigger you get, the smaller the opportunity set. If you find smaller ideas, you still have to find more of them.

Some of this is also due to the low interest rate environment post-crisis and the rush of investment capital into alternatives that serve to tighten spreads and lower returns.

I don't know how much of recent returns are due to each of these factors, so it's hard to tell how things will unfold going forward.

But I do like the strategy mix, at least of the main strategies (excluding credit/real estate). Those strategies are typical of the pre-Dodd/Frank equity proprietary trading desks at the investment banks. They don't involve forecasting/guessing about the markets, economy or anything like that. They are usually spread trades (risk arbitrage, convertible arbitrage etc...).

It's possible that there is so much capital chasing those deals that returns won't go back to what they were years ago. But also, a lot of the spread compression is due to lower interest rates (if your carry costs go down, you can obviously pay a higher price in a risk arb trade, for example).

Low Returns in Context

Having said all that, we have to look at this in context. 10-year treasury yields are 2.2%, the earnings yield on the S&P 500 index is around 5%, and the expected return in stocks using Buffett's old metric is 6.2% or so (he has said more than once that expected returns in stocks is the dividend yield plus inflation plus real economic growth rate: 2.2% dividend yield + 2.0% real GDP growth + 2.0% inflation = 6.2% expected return for stocks).

6-8% returns for OZM funds in this environment is not bad at all. Keep in mind their low beta on the downside; the stock market might have 5-6% prospective returns, bonds might yield 2.2%, but the stock market can have painful bear markets and if interest rates go up, losses in bonds can be pretty painful too. OZM has shown that in down markets they outperform handily.

So one can ask, is it better to expect 6-8% returns from OZM funds with some downside protection, or should we go with 5-6% expected returns in the stock market with the inevitable, occasional 50% drawdowns? Or should we invest in bonds for a 2.2% yield and a possible bloodbath when rates start to rise? Or should we sit on 0% interest rates until the Fed really normalizes?

None of this is my opinion; just the possible thought process of an investor in OZM funds.

When you look at it like this, the low returns don't look so bad. Also, there is the optionality to the upside. When markets return to a more chaotic environment (instead of the low volatility environment we've seen post-crisis), spreads may widen, opportunities increase and returns can improve.

In that sense, OZM funds don't look so bad at all.

Or you can take a look at OZM itself and shoot for 10% returns (but with the above-stated risks).

Conclusion

Well, I don't really have a conclusion here. It's certainly interesting and cheap. OZM is a really great shop as far as I know, and I like the mix of their strategies. But the two issues are the lower recent returns and the ongoing dilution that seems to really dampen the upside; if OZM has a great year, who knows how many RSU's and Group A units they will grant to their employees?

On the other hand, it looks like OZM yields 10%+ whether they do really well or have a so-so performance year like last year.

So would you be better off investing in OZM for that 10+% yield instead of the 6-7% return in the OZM funds? Of course this would not be practical for large institutions, or investors who have a large portion of their net worth tied up in the funds.

Normalizing interest rates (which look more and more further out every day), like with so many other financials, will certainly help OZM as spreads will no doubt widen in the various strategies.

Other alternative managers are getting really cheap now too so I will be taking a look at those over the next few weeks.

Stephen Schwarzman of Blackstone (BX) has been frustrated with a cheap stock price for a long time now, and it's just getting cheaper. BX is sort of the gold standard in private equity. Schwarzman says that Wall Street doesn't get it, that BX is like LeBron James. But what investors fear is that BX is like LeBron James, but that every time he scores, the ball gets a little bit bigger so each prospective point gets harder and harder.

There is no doubt that things are getting cheap in the sector.

If there is a credit event (Glencore bankruptcy?), though, financials can all get hit hard as nobody will really know who is holding the bag so one would have to be cautious.

Private equity needs a good credit market and good 'exit' market. But of course, these things go through cycles and without bad times, they won't be able to put big amounts to work for high returns. The fear is, I suppose, that these stocks get hit really hard in the down cycles.

I do think the good private equity firms will continue to do pretty well through the cycle. It's how much stomach do you have to sit through the down cycles? Anyway, maybe I'll look at some of that stuff later.

This is one aspect that interested me with OZM. They are not private equity, so as long as they retain/increase AUM, they should do well.

I also understand that there is an investigation and that some pension funds are pulling out of hedge funds due to low returns. These don't overly concern me. Pension fund investing goes through cycles too. There was a big boom in hedge fund investing after the crisis, and that is sort of unwinding. Pension funds are rear-view mirror investors, so what they do doesn't concern me too much. In fact, I don't mind at all going the other way.